VC investment in low-carbon hydrogen technology rose from around $600 million in 2022 to $1.5 billion in 2023 (Oliver Wyman, 2024). This is understandable. Global hydrogen production stands at approximately 100 million metric tons annually, with about 95% being used in “hard to decarbonize” industrial processes from ammonia and methanol production to oil refining (hydroprocessing) and metalworking (IEA, 2023). Much of this capital has been invested in green hydrogen startups which pursue advancements in hydrogen electrolysis (splitting water with electricity to produce hydrogen) using renewable energy. Today, green hydrogen production accounts for only 1% of the entire $100bn hydrogen production market (EEIS, 2022). The reason for this is actually quite simple - green hydrogen is far too expensive even with government subsidies and the lower cost of solar.

Percent of Hydrogen Demand Globally

Source: IAE, 2022

Going forward, we believe early stage venture capital dollars in the hydrogen economy should no longer target green hydrogen startups. Instead, we believe vertical integrators that incorporate clean hydrogen production within a broader industrial process will drive better returns. This is because long-distance, low-cost transportation of hydrogen remains an unsolved problem. For example, existing gas pipeline infrastructure quickly degrades when exposed to hydrogen. This forces hydrogen production to be located where it’s consumed.

Furthermore, we believe the investment ecosystem is still under estimating the potential of nuclear-powered hydrogen electrolysis (pink hydrogen) and thermolysis (purple hydrogen) to enable cost-competitive clean hydrogen production at scale, especially when pursued within a vertical integrated model.

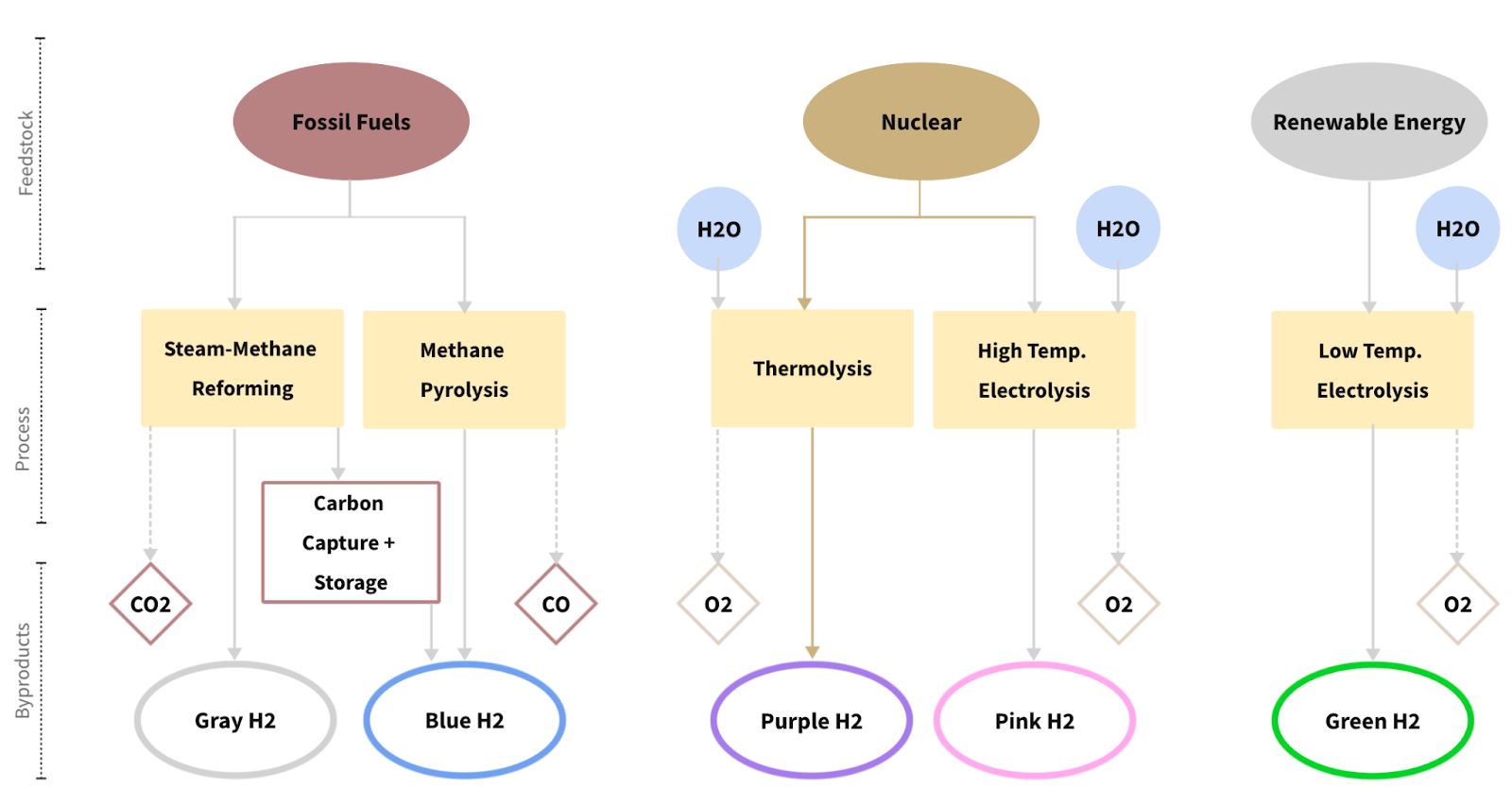

Leading Processes for Hydrogen Production

Source: Lazard’s Levelized Cost of Hydrogen Analysis

The Electrolysis Conundrum: Why Green Hydrogen Struggles to Compete

While renewable powered, electrolysis-based hydrogen production has garnered significant attention and investment, it faces substantial challenges in achieving cost competitiveness against incumbent industrial hydrogen production methods:

- Entrenched Competition: Most existing industrial sites already utilize cheap but dirty steam methane reforming (SMR) for hydrogen production. These facilities have already claimed the scarce asset of proximity, minimizing transportation and compression costs.

- Costly Retrofits: For green hydrogen to penetrate these markets, it requires expensive retrofits of existing industrial processes optimized for SMR. Electrolysis and SMR are completely different systems that produce hydrogen at different temperatures and pressures. This additional capital expenditure further erodes the economic viability of electrolysis-based hydrogen on existing industrial sites.

- Off-site Production Challenges: If green hydrogen production is forced off-site due to space constraints or other factors, it immediately loses any potential for cost competitiveness. The added expenses of compression, transportation, and storage prices it out of the market. It's akin to baking bread in one city and trying to sell it fresh in another – possible, but rarely economical.

To illustrate this point, let's consider the economics:

- Compression costs: Compressing hydrogen to 350-700 bar for transportation can consume 10-15% of the hydrogen's energy content. (Franco, Giovanni, 2024)

- Transportation costs: Trucking compressed hydrogen costs at least $2-$3 per kg. (UC Davis, 2024)

- Storage costs: Large-scale hydrogen storage facilities can cost $500-$1000 per kg of storage capacity. (Moran, 2024)

These factors combined can double to triple the cost of hydrogen, which is significant when competing against on-site steam methane reforming (SMR) that produces hydrogen at $1-$2 per kg (University of Alberta, 2024). The economic viability of off-site electrolysis is thus severely constrained, limiting its market penetration to currently niche applications (mobility) or heavily subsidized environments.

- Intermittency Issues: In industrial settings, high utilization rates are crucial to justify the substantial fixed costs associated with large-scale facilities. The intermittent nature of renewable energy sources poses a significant challenge for electrolysis-based hydrogen production. Industrial operations cannot afford "stranded capital" – expensive equipment sitting idle due to fluctuating energy supply (e.g. sun is not shining, wind is not blowing). The costs associated with firming renewable energy sources to ensure consistent production are prohibitively high, further eroding the economic viability of green hydrogen in industrial applications.

These factors collectively create a formidable barrier for electrolysis-based hydrogen production in competing with existing SMR facilities that could integrate carbon capture and sequestration technologies. The promise of green hydrogen, while appealing from an environmental standpoint, faces an uphill battle in achieving economic viability in industrial contexts today.

Nuclear-Powered Hydrogen: The Overlooked Enabler

By leveraging nuclear power for hydrogen production, we could overcome the economic hurdles that have kept clean hydrogen from being competitive with SMR-produced hydrogen, opening up new possibilities for industrial decarbonization.

Nuclear-powered hydrogen production can be achieved through two main methods: electrolysis (pink hydrogen) and thermolysis (purple hydrogen). Hydrogen thermolysis is a process that uses very high temperatures (~900°C or more) to split water molecules directly into hydrogen and oxygen without the need for electricity.

Unlike renewables that cannot efficiently produce this high temperature heat, advanced reactor designs like high temperature gas reactors (HTGRs) produce heat nearing ~1000°C. Nuclear systems solely targeting heat will also be cheaper to build and easier to operate than their electric counterparts as they will not require turbines.

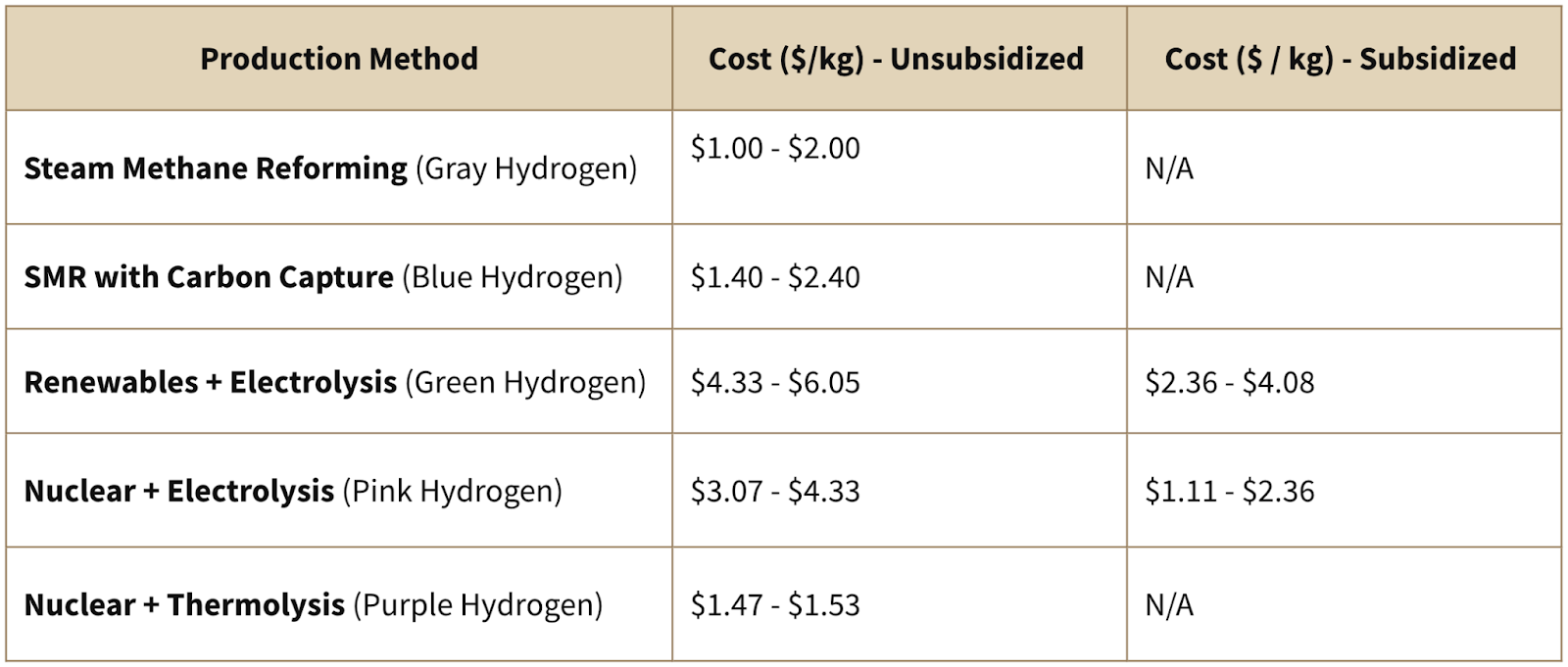

Let's examine the cost profiles of these methods for the US market:

Source: Lazard’s Levelized Cost of Energy Version 17.0 (2024), and General Atomics Report - Large-Scale Production of Hydrogen by Nuclear (2003)

Nuclear production methods offer several advantages:

- Cost Efficiency: Nuclear-powered hydrogen production, particularly thermolysis, has the potential to be highly cost-competitive, with purple hydrogen potentially achieving sub-$1 per kg costs. This is significantly lower than both green hydrogen ($4.3-$6.1 per kg) and current SMR-produced hydrogen (typically $1-$2 per kg). This is because nuclear reactors produce high-temperature heat, which can be directly used in more efficient thermolysis or high-temperature electrolysis, improving overall system efficiency. Renewable energy sources typically only provide electricity, losing the potential benefits of heat integration.

- High Capacity Factor: Nuclear plants typically operate at capacity factors above 90%, ensuring consistent hydrogen production for direct integration into industrial applications. This can justify the high capex amortized over many years and is crucial for project finance.

- Space Efficiency: Nuclear-powered hydrogen production can be co-located with industrial facilities, minimizing transportation costs and losses. Renewable energy sources often require significant land area, which may not be available near industrial centers. Nuclear-powered hydrogen production requires significantly less land area compared to solar or wind-powered electrolysis for equivalent hydrogen output.

The caveat with nuclear power is regulation. In the past, this has meant the idea of nuclear-powered hydrogen production was dead on arrival. However, we believe there is a growing recognition of the need for nuclear as clean, baseload power globally. In Switzerland for example, where our nuclear company Transmutex is based, there will be a referendum to overturn the ban on new plants. In the US, there was bipartisan support for the ADVANCE Act designed to streamline nuclear licensing. Furthermore, nuclear has become a key talking point in the 2024 Presidential Election, which we discussed live on Bloomberg TV.

General Partner, Cameron Porter, Bloomberg Interview

The potential for sub $1 per kg hydrogen production via nuclear thermolysis is particularly noteworthy, as it would represent a step-change in the economics of clean hydrogen production. This could significantly accelerate the adoption of hydrogen in various industrial processes and potentially open up new use cases where hydrogen is considered too expensive, like hydrogen fuel cells for mobility.

Natural (white or gold) hydrogen is also a potential source that could reach the sub $1 per kg threshold. However, this approach requires significant transportation costs as supply will not be co-located with demand. This will limit its viability as a large-scale solution for industrial applications.

The Benefits of Vertical Integration as a Venture Investment Strategy

We believe the most promising investment opportunities are not in pure-play hydrogen synthesis, but in vertically integrated industrial operations that utilize hydrogen as a key input. Friend of the fund Packy McCormick of popular technology blog Not Boring recently wrote an exceptional piece on why vertical integrators will be the biggest winners in industrials. Building on Packy’s thinking, we see the most important benefits of this vertical integration strategy as:

- Integration of multiple advanced, proven technologies: Vertical integration allows companies to combine various cutting-edge technologies across the value chain, creating unique and powerful solutions that are difficult for competitors to replicate.

Example: SpaceX extensively uses 3D printing technology, which was developed in other industries, for manufacturing complex rocket components. They use this technique to produce parts like the SuperDraco engine chamber for the Dragon spacecraft and other intricate components. - Development of multiple in-house capabilities: By controlling multiple stages of production and distribution, vertically integrated companies can develop deep expertise in all aspects of their business, leading to continuous improvements and innovations.

Example: SpaceX controls multiple stages of production, from design of its Raptor engines to assembly. - Modularization of commoditized components while maintaining control over system integration: This approach allows companies to benefit from cost reductions in standardized components while still maintaining a competitive edge through superior system integration and optimization.

Example: While SpaceX designs and builds many components, it also outsources tens of thousands of parts to suppliers. This approach allows them to benefit from cost reductions in standardized components while using in-house capabilities where it makes sense.

These advantages enable vertically integrated companies to deliver products that are superior in quality, speed, or cost-effectiveness, often achieving all three simultaneously. In the case of industrials using advanced integrated hydrogen production, this can mean delivering a premium green product profitably at commodity prices.

It's worth noting that there has been a trend towards modular, decentralized production in chemical manufacturing. Although we view this as a form of "miniaturized vertical integration." BASF, Bayer, Merck and others are all involved in a modular plant working group. This approach has seemed attractive due to the ability to place production facilities near renewable energy sources or demand centers. However, we remain skeptical of its long-term price competitiveness due to the economies of scale achieved by large, centralized production sites.

We believe that for clean hydrogen to reach scale, it requires operating as a vertically integrated industrial company. In this context, nuclear-powered hydrogen production (whether through thermolysis or high-temperature electrolysis) makes more sense than electrolysis with renewables.

Vertical Integration for Clean Hydrogen Enabled Industrial Products

Hydrogen production can be seamlessly integrated into various industrial processes to create clean versions of traditional products. Some examples include:

- Green Steel Production: By using hydrogen as a reducing agent instead of coal in the iron ore reduction process, steel manufacturers can significantly reduce their carbon emissions. A vertically integrated operation could include on-site nuclear-powered hydrogen production, direct reduced iron (DRI) facilities, and electric arc furnaces, resulting in high-quality, low-carbon steel. The elephant in the room is H2 Green Steel (raised over $5b in funding) with the goal of producing 5m tonnes of hydrogen green steel per year by 2030.

- Carbon-neutral Cement Manufacturing: Integrating hydrogen production with cement kilns can allow for the use of hydrogen as a fuel source, dramatically reducing CO2 emissions. The integration could also include carbon capture and utilization technologies, using the captured CO2 in combination with hydrogen to produce synthetic aggregates or other valuable products. Cemex, one of the world’s largest cement producers, is implementing hydrogen injection technology at 4 of its plants in Mexico.

- Synthetic Aviation and Diesel Fuel: Combining hydrogen production with carbon capture technologies enables the creation of synthetic fuels through processes like Fischer-Tropsch synthesis. A vertically integrated operation could produce hydrogen, capture CO2 from industrial processes or the air, and synthesize drop-in fuels that are chemically identical to conventional jet fuel or diesel but with a significantly lower carbon footprint and less impurities like sulfur. Honeywell, Air Products, and others are building North America’s largest synthetic aviation fuel (SAF) plant using hydrogen. By 2050 the facility will produce fuels that will displace over 76m metric tons of CO2, the equivalent of 3.8m carbon-net-zero flights from Los Angeles to New York.

- Clean Chemicals Production: Many chemical processes rely heavily on hydrogen as a feedstock. The chemical industry operates on a global scale, processing millions of tons of material annually. Its outputs – ranging from paints and plastics to fertilizers – are deeply embedded in countless high-volume products that shape our daily lives. By integrating nuclear-powered hydrogen production with chemical synthesis operations, companies can produce a wide range of products - from ammonia and methanol to plastics and pharmaceuticals - with dramatically reduced carbon emissions. Green Ammonia by Haldor Topsoe is a massive producer based on green hydrogen and nitrogen that was just inaugurated in Denmark.

In each of these examples, vertical integration allows for optimized process design, reduced transportation and storage costs, and the ability to capture value across multiple stages of production. This approach not only improves the economics of clean hydrogen utilization but also creates barriers to entry for potential competitors.

Conclusion

Investors can better position themselves to capitalize on a significant blindspot in the current market by focusing on vertically integrated solutions that leverage nuclear-powered hydrogen synthesis. This approach not only addresses the key challenges faced by electrolysis-based systems, but also offers a clean alternative to SMR. By combining vertical integration with nuclear-powered hydrogen production, this strategy presents a viable path to achieving both economic viability and environmental sustainability in the emerging hydrogen economy.