Valar Atomics is pioneering a breakthrough in energy by combining proven High-Temperature Gas Reactor (HTGR) technology with a novel business model to create synthetic, net-zero fuels. Led by Isaiah Taylor, an autodidact and serial entrepreneur, and supported by Chief Nuclear Officer Mark Mitchell, a leading expert in TRISO-fueled reactor design, Valar’s integrated approach removes traditional barriers to scaled reactor-deployments by producing and using its own reactors to drive down costs. With the potential to disrupt both energy and industrial sectors in need of high temperature heat, Valar is poised to deliver clean, competitively priced synthetic fuels at scale—unlocking a trillion-dollar opportunity in the global energy market.

The Nuclear Renaissance

We stand at the threshold of a nuclear renaissance that promises to revolutionize global energy production. Where others see challenges, we see a unique opportunity to provide cheap, clean, and reliable energy at a scale necessary to power a growing, energy-hungry world. Nuclear fission is uniquely positioned to address the shortcomings of intermittent renewable sources, which struggle to meet the consistent energy demands of industrial economies. Advanced reactor designs, capable of producing high temperatures, are not just a replacement for fossil fuels—they can reshape the energy landscape entirely by enabling carbon-neutral fuels, such as synthetic hydrocarbons and hydrogen, to become economically viable.

This renaissance is not about incremental improvements but about fundamentally shifting the energy paradigm. While much of the venture ecosystem focuses on small modular reactors (SMRs) for electricity generation, the true potential of advanced reactors lies in their ability to provide high-temperature heat. This is the key to decarbonizing heavy industries like steel, cement, and petrochemicals, which account for nearly a third of global emissions and cannot be easily electrified. Advanced reactors, particularly High-Temperature Gas Reactors (HTGRs), can provide the zero-carbon heat necessary to replace fossil fuels in these critical sectors.

Nuclear heat represents the untapped frontier, one capable of transforming industries and propelling decarbonization far beyond what renewables can achieve. The opportunity for nuclear energy today is vast, but few truly see the full scope. By combining advanced reactor technologies with innovative business models, nuclear power can usher in an era of clean, affordable energy, unlocking industrial decarbonization on a global scale. This is the future that awaits those bold enough to invest in and champion nuclear’s potential.

The VC Trap — Light Water Reactors Will Win In Electricity

Despite the benefits of passive safety systems and claims of lower levelized costs of electricity (LCOE), we believe the advanced designs for small modular reactors (SMRs) pursued by many startups will not be able to compete with incumbent large-format light water reactors (LWRs) nor their scaled-down light water SMRs in supplying electricity to the grid. The key reasons for this are the following:

- Entrenched Ecosystem: Established reactor vendors have locked in multiple pieces of the value chain. More government dollars flow towards LWRs than advanced reactors. Regulators base their approvals on precedent that mostly comes from LWRs. Utilities optimize their choice to align with regulator preferences. Shared supply chains drive down costs.

- Unaccounted for Costs: LCOE does not account for standardization around LWRs. For example, the internal costs of multi-annual technical due diligence and operator training that standardized best practices have decreased by over 30% in the last decade for LWRs.

- Business Model Deficiencies: Incumbent LWR vendors earn revenue from more than just electricity or reactor design licenses, they provide components, fuel, services, and plant equipment. When they sell a reactor, these firms generate revenue at each phase of the reactor's lifecycle (procurement, construction, licensing, fueling, maintenance, etc).

MIT’s Advanced Nuclear Power Program’s, Dr. Koroush Shirvan, supports the conclusion that large-format LWRs, specifically Westinghouse’s AP1000, will outcompete SMRs and renewables in terms of conclusion in his July 2024 report comparing the AP1000 to renewables and SMRs concluding the, “AP1000 will provide similar generation cost as the current ~$65/MWhre electricity generation cost … This means deep decarbonization can economically be done with AP1000 while alternatives will only raise the cost of electricity” (Shirvan, 2024).

Nuclear Heat — The Real Opportunity for Advanced Reactors

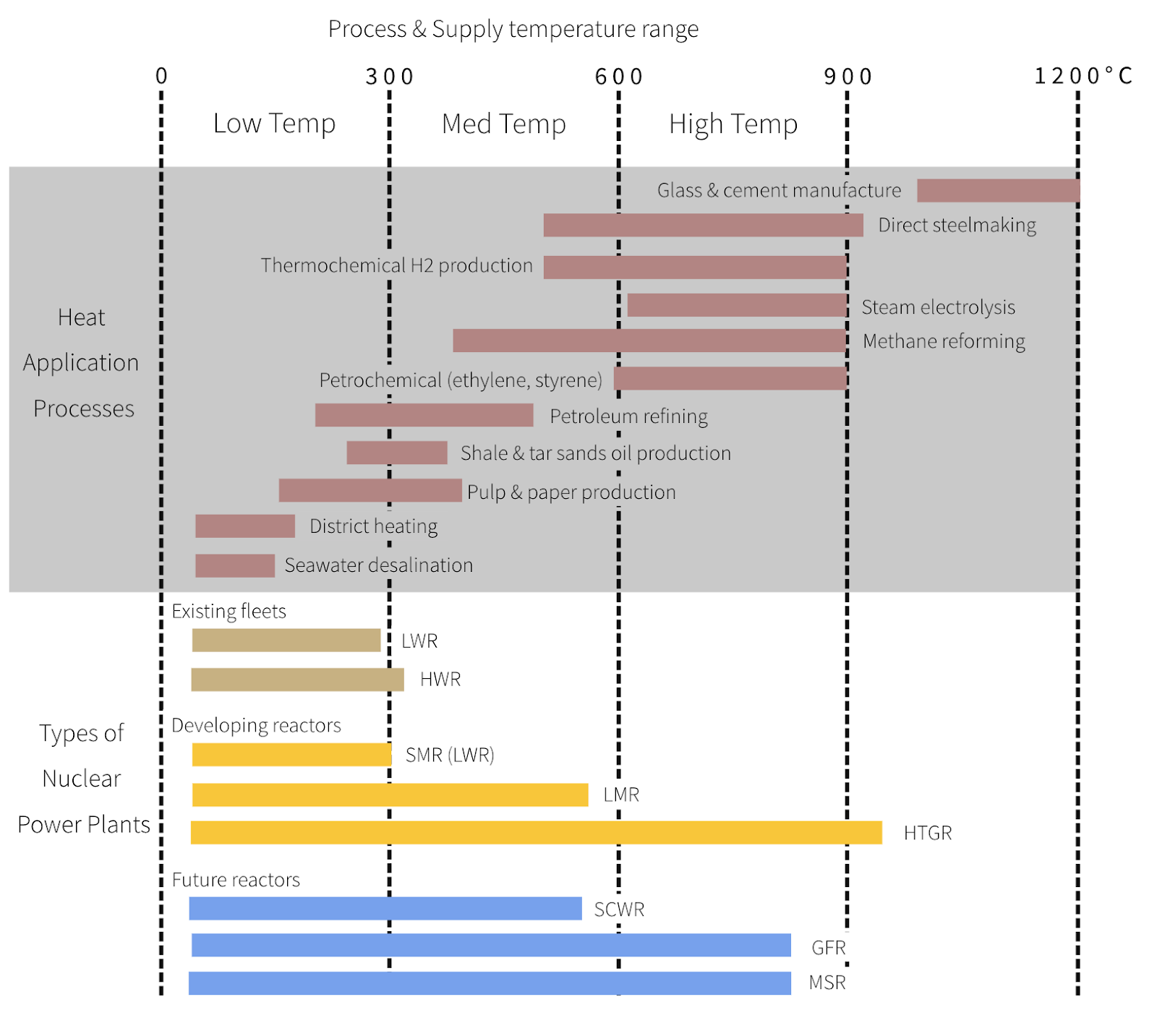

Heavy industries (cement, steel, and petrochemical production), air travel and freight shipping account for roughly 30 percent of global CO2 emissions (Greene, 2023). These industries are notoriously difficult to electrify as they require the creation of tremendously high heat (600°C - 1000°C) for extended amounts of time. Though it is theoretically possible to make these processes electric, it is extremely uneconomical to do so (Friedmann et al, 2019).

Advanced reactors can make zero-carbon high heat economically competitive with natural gas, coal, and oil methods. Although molten salt, sodium-cooled, liquid-metal cooled, and other advanced reactor designs can all produce heat in excess of 500°C, high temperature gas reactors (HTGRs) are the optimal design when heat production is your primary (or only) objective. Notably, LWRs are not competitive in this domain as they are only capable of producing up to 300°C.

Reactor Types and Industrial Heat Applications

HTGRs, which use helium as coolant, can not only produce heat in excess of 950°C, their safety profile makes them ideal relative to other reactor designs for co-location with other industrial processes. Furthermore, designing a reactor for heat production only has cost benefits. Power in the form of heat can be much cheaper than electric power because there is no power conversion loss and no capital investment in expensive turbine-generators. It is rarely recognized that 1 joule at 900°C is more valuable than 1 joule at 350°C. This is precisely what HTGRs can deliver.

HTGRs have been built and operated for over 50 years. Central to these reactors is the use of TRISO fuel, a meltdown-proof, highly durable, and proliferation-resistant fuel that has been utilized in more than 30 grid-scale reactors since the 1960s. In an industry where safety and regulation are paramount, the long history and proven success of HTGRs provides a strong foundation for advancements in this reactor design.

The potential to use nuclear for high temperature heat is still virtually unknown to the public, politicians, and even many venture investors. We see a path for high temperature from purpose-built HTGRs costing less than $0.01/kWh. This type of cheap, clean, heat would unlock new use cases. High temperature heat can efficiently break hydrogen out of water (thermolysis), heat buildings, power electrochemical separators to capture carbon-dioxide, and enable refineries to produce net zero fuels.

Hydrogen — High Heat’s Biggest Unlock

The venture ecosystem already recognizes the upside for any technology that can produce cheap hydrogen at scale. VC investment in low-carbon hydrogen technology rose from around $600 million in 2022 to $1.5 billion in 2023 (Oliver Wyman, 2024). Global hydrogen production stands at approximately 100 million metric tons annually, with about 95% being used in “hard to decarbonize” industrial processes from ammonia and methanol production to oil refining (hydroprocessing) and metalworking (IEA, 2023).

Hydrogen Demand Globally

Much of this capital has been invested in green hydrogen startups which pursue advancements in hydrogen electrolysis (splitting water with electricity to produce hydrogen) using renewable energy. However, green hydrogen production accounts for only 1% of the entire $100B hydrogen production market (EEIS, 2022).

The reason for this lack of market penetration is simple: green hydrogen is too expensive even with government subsidies and the declining cost of solar. The energy return on investment (EROI) of hydrogen production is not efficient. Current processes yield between a quarter or a fifth of the energy invested in harvesting the hydrogen, and until this improves, the hydrogen economy will likely be a non-starter.

However, by leveraging direct nuclear heat for hydrogen production, we could overcome the economic hurdles that have kept clean hydrogen from being competitive with hydrogen produced via steam-methane-reforming, opening up new possibilities for industrial decarbonization.

Hydrogen Cost Comparison by Technology

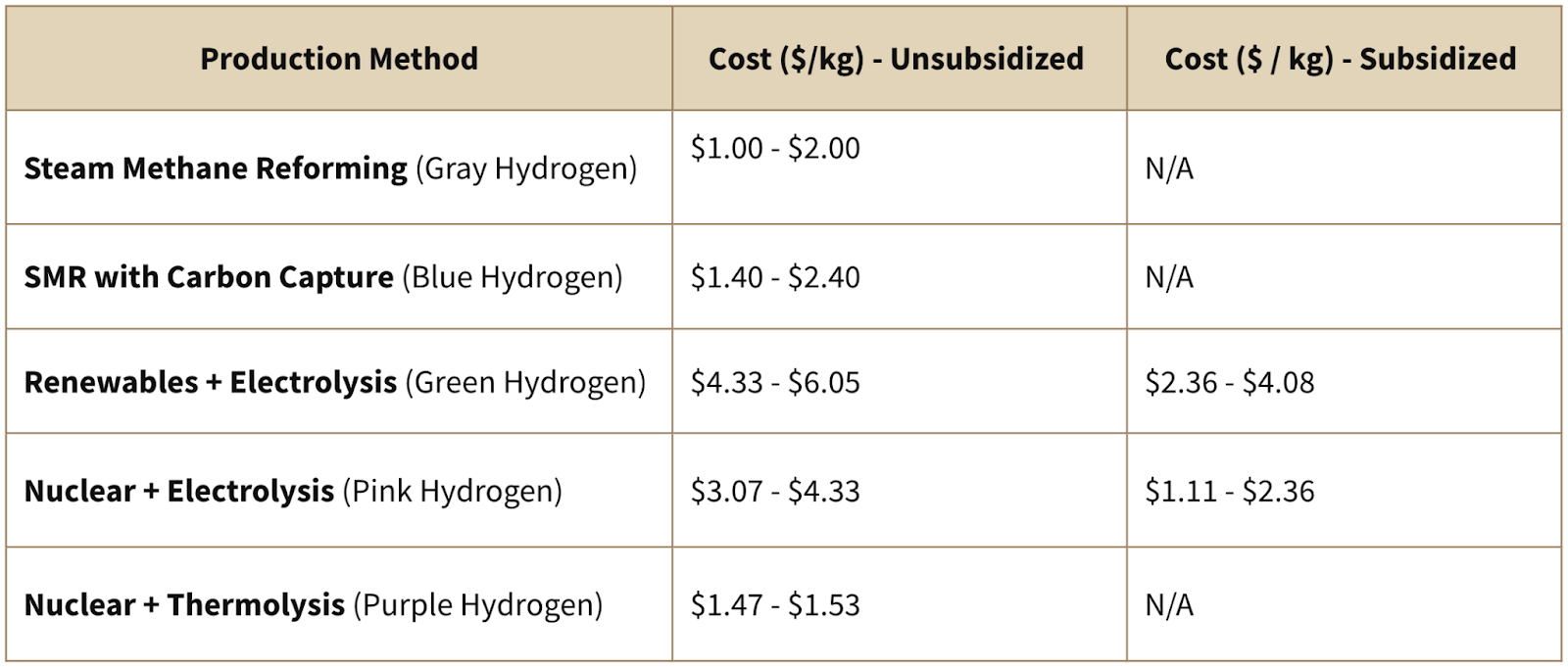

Nuclear-powered hydrogen production can be achieved through two main methods: high temperature steam electrolysis (pink hydrogen) and thermolysis (purple hydrogen). Hydrogen thermolysis is a process that uses very high temperatures (~800°C or more) to split water molecules directly into hydrogen and oxygen without the need for electricity. Thermolysis is theoretically cheaper than electrolysis because it does not require inefficient conversions of heat power to electric power or vice versa.

Of the potential methods of hydrogen thermolysis, the sulfur-iodine (SI) cycle is one of the most efficient with a potential thermal efficiency of up to 50%. The Japanese Atomic Energy Association (JAEA) has already demonstrated efficiencies of 40%. Despite the potential to deliver a breakthrough in low-cost, clean hydrogen, the SI process has remained underexplored in the commercial landscape with the notable exception of General Atomics in the early 2000s.

We believe this lack of commercial interest has been driven by two factors. The first is concerns around the feasibility of constructing commercial scale SI cycles given the requirements for materials to handle high temperature, corrosive chemical environments. The second is the inaccessibility of cheap, clean 850°C+ heat.

As of today, these two factors blocking the viability of commercial SI can be solved for. First, the JAEA recently demonstrated that steel alloys, which are well suited for commercial scale facilities, have corrosion resistance on par with the non-scalable ceramics used in the past (JAEA, 2021). Second, as covered in the nuclear heat section, we see a path to deploying HTGRs for industrial heat provision.

Given these developments, we believe that the combination of SI at 30% thermal efficiency and 850°C+ heat from mass-producible HTGRs provides an achievable pathway to sub $1 per kg hydrogen. This achievement would be a breakthrough in the hydrogen economy, outcompeting dirty steam-methane-reforming. Beyond that, sub $1 per kg hydrogen would unlock the ability to produce net-zero hydrocarbon fuels (diesel, gasoline, jet fuel, etc) at prices competitive with traditional fossil fuels.

Cheap, Clean Synthetic Hydrocarbon Fuels

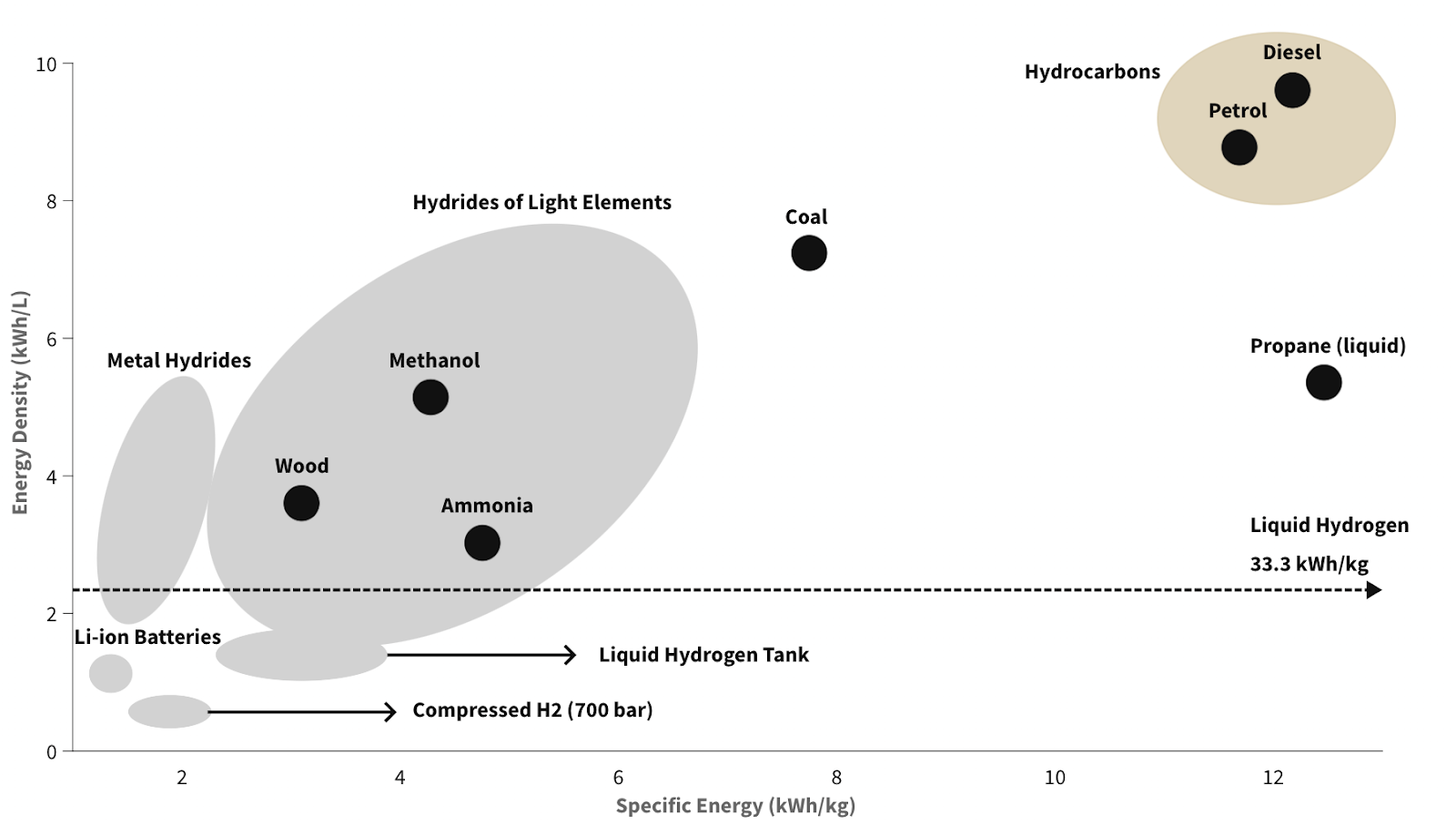

To date, more than 80% of the global primary energy demand is based on fossil fuels, in particular crude oil. Fossil fuels (long-chain hydrocarbons) represent an ideal energy carrier. They store energy in their carbon-carbon or carbon-hydrogen bonds and release this energy through combustion. In terms of weight, energy density, and ease of transportation, long-chain hydrocarbons are the most efficient and economical fuel we have. These fossil fuels benefit from decades of large-scale investment across the value chain, from extraction and refining to transportation and consumption via combustion.

Hydrocarbons are an Optimal Fuel

Increased consumption of fossil fuels is among the primary forces of global economic growth. However, their extensive use is an ongoing source of volatility due to both climate change from greenhouse gas emissions and geopolitical tensions from relative resource scarcity. If you could profitably produce hydrocarbon fuels anywhere in the world without increasing carbon-dioxide emissions, you could build one of the world’s leading energy companies.

Based on the ability to produce clean hydrogen at ~$1-2 per kg with the SI cycle powered by HTGR heat, we believe there is a credible path to net-zero hydrocarbon fuels using proven techniques. Oil refineries have demonstrated at commercial scale that they can produce synthetic crude oil (syncrude) from syngas (carbon monoxide + hydrogen) using the Fischer-Tropsch process (FT). SASOL in South Africa has produced 160,000 barrels of syncrude per day using this technique. However, this is achieved by using dirty coal gasification to produce cheap syngas.

Clean, low-cost syngas could instead be produced by combining hydrogen from nuclear powered thermolysis with carbon-dioxide from carbon-capture-and-sequestration (CCS) at natural gas or coal power plants using a reverse-water-gas-shift reaction (RWGS). Eventually, global investment in and scaled deployment of direct-air-carbon capture (DAC) could produce low-enough cost carbon for use in synthetic fuel production as well. With ~$1-2 per kg hydrogen and ~$0.05 per kg carbon-dioxide, we believe that a barrel of net-zero synthetic fuel could be produced from syncrude at below $85 per barrel using FT. This would be competitive with global fossil fuel supplies.

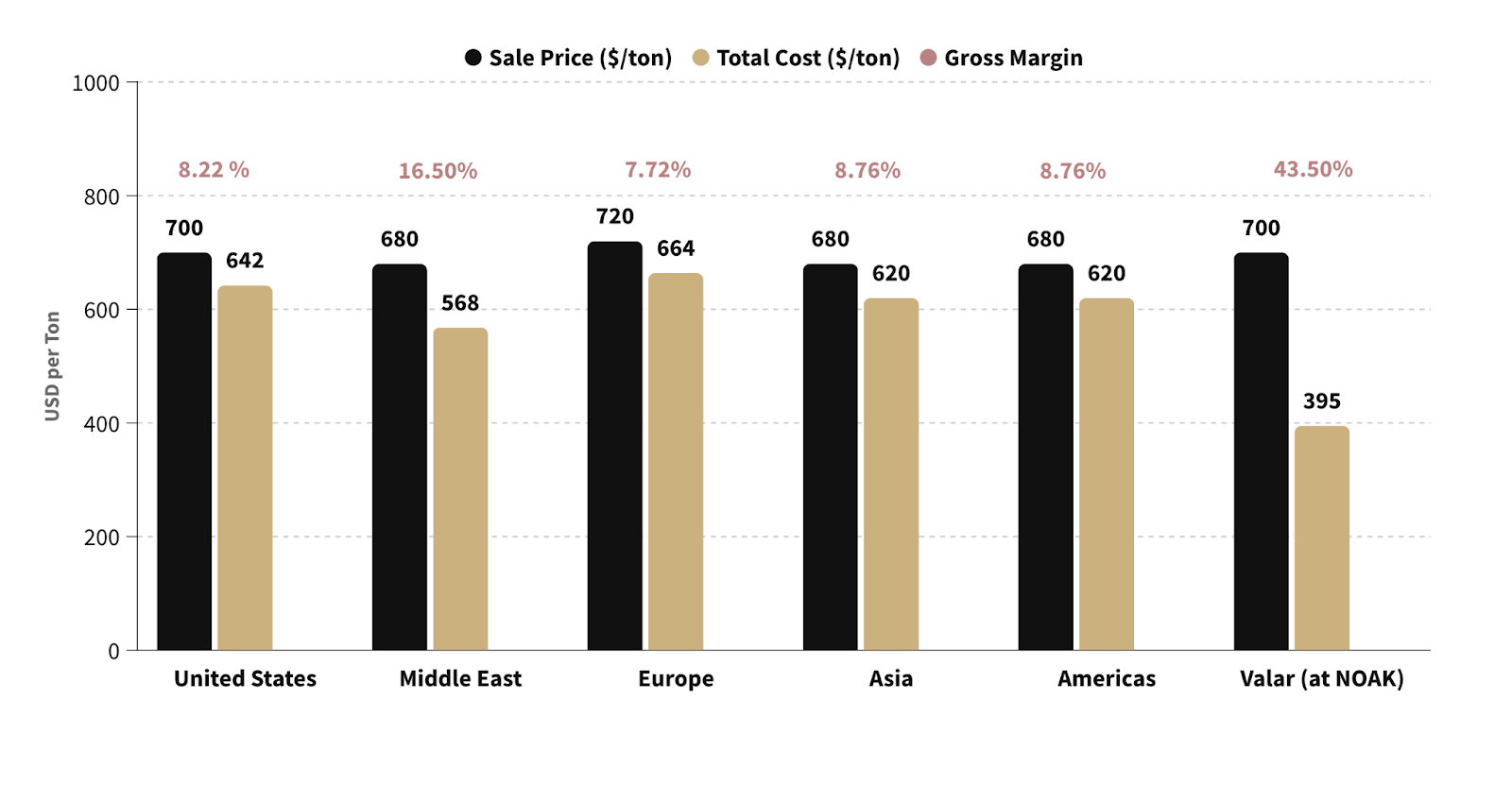

Oil Refinery Economics

Once syncrude is produced, existing refining processes can be used to produce valuable end products (diesel, gas, jet fuel, etc). In fact, due to the higher purity of syncrude, these net-zero synthetic fuels should not only be easier to produce but also of higher quality than their fossil fuel counterparts.

Finally, given the expectation that the EROI (the amount of usable energy produced in relation to the amount of energy used to create it) of oil continues to increase overtime, having gone from 100:1 in the late 1800s to between 4:1 and 30:1 across the global market (JPT, 2023), as well increasing long-term oil demand predictions, we believe $60-90 per barrel syncrude will be price competitive with crude oil in the decades to come. Based on this analysis, we believe there is a durable opportunity to produce net-zero fuels using existing technologies as an integrated industrial process.

Valar’s Winning Formula

Valar Atomics, led by Founder / CEO Isaiah Taylor and Chief Nuclear Officer (CNO) Mark Mitchell, is capitalizing on this realization that net-zero hydrocarbon fuels produced at competitive prices is within reach by driving down the cost of constructing HTGRs.

To achieve this, Valar has developed an integrated business model that avoids the challenges that will continue to prevent other advanced reactor companies from reaching the scaled deployments (100s of reactors) that would justify mass manufacturing. It is only through centrally manufacturing HTGRs that we will be able to achieve the cost of heat necessary for hydrogen production via SI cycle.

Instead of selling their HTGRs to a third-party, Valar is designing and building their own integrated process for synthetic fuel production (nuclear heat → SI cycle → FT process → fuel refining) on a single industrial site called a “Gigasite”. Through this Gigasite model where Valar could have ~100 reactors at a single location, Valar gains two key advantages relative to other reactor companies. First, they become their own customer for their reactors. Second, they minimize their regulatory burden and licensing costs.

Sell Fuel Not Reactors

By becoming the customer for their own complex technology (HTGRs) that deliver a simple product (heat), Valar avoids having to sell a complex technology to customers with entrenched interests (utilities) or customers with limited ability to evaluate the technology (industrial plants). In doing so, Valar is following in the footsteps of companies like SpaceX. SpaceX became the customer for their complex technology (rockets) that delivers a simple product (kg of payload to space) by developing Starlink, a satellite constellation that can deliver high-speed internet across the globe.

This approach minimizes the number of third-parties involved in Valar’s reactor deployments and allows Valar to directly benefit from improvements in their reactor design in terms of lower synthetic fuel COGS. Just as SpaceX can sell internet around the globe without needing to explain their rockets to a customer, so will Valar be able to sell their fuels without needing to explain their reactors.

Rendering of Valar’s System

Amortize Licensing Costs

Building a nuclear reactor involves navigating a complex array of regulatory and licensing burdens designed to ensure safety, environmental protection, and security. These include obtaining approval from national nuclear regulatory bodies, such as the Nuclear Regulatory Commission (NRC) in the United States, which oversees the reactor’s design, construction, and operation. The process typically involves a rigorous review of the reactor’s safety systems, environmental impact assessments, and emergency preparedness plans.

Additionally, site-specific licenses must be obtained, often requiring local and state government approvals. There are also extensive requirements for public consultations, adherence to international non-proliferation agreements, and securing liability insurance under frameworks like the Price-Anderson Act. Each step of the process is designed to mitigate risks and ensure that the reactor can operate safely within all regulatory guidelines.

By concentrating reactor deployment to Gigasites, Valar will minimize their regulatory burden by amortizing the site-specific licensing costs over 10x-100x more reactors than compared to other reactor companies. This will allow local regulators and politicians to build familiarity with the systems as the deployment scales versus having to continuously educate stakeholders in new locations. Furthermore, Valar will be able to build up a skilled labor force at the site, avoiding excess costs of labor procurement and training for the complexities of nuclear construction and operation.

It Only Takes One

Selling electricity is a demand constrained environment. You can only deliver electric power to customers within a localized geography via the grid or potentially even a single customer “behind the meter”. Selling electricity using reactors puts a cap on the number of reactors that can be deployed per site. Valar’s approach eliminates this constraint.

Unlike with electricity, the market and supply chain for diesel, gasoline, jet fuel, etc is structured such that local supply can meet demand wherever it is in the world. This means that as long as the site can produce fuel at a competitive price, the market will be able to match that supply to demand. Thus barring site specific constraints, Valar will be able to incrementally grow their synthetic fuel output by deploying more HTGRs. This will drive down costs via both amortized licensing and scaled manufacturing, making their fuels even cheaper. These lower prices will unlock new demand thereby justifying more HTGRs and so on.

The key to unlocking this virtuous cycle of declining costs from manufacturing driven learning curves is if Valar can produce a single 75 MWth HTGR with a low enough overnight construction cost to produce competitively priced synthetic fuels without subsidies. Assuming a barrel of fuel sells for $80-90, 30% thermal efficiency SI cycle, 10% interest rate, and operating costs on par with existing LWRs, this would require Valar to build a 75 MWth HTGR with an overnight construction cost of ~$40-50M or a levelized cost of energy of ~$15-20 per MWh(th).

For comparison with other advanced reactors that quote a levelized cost of electricity, we can assume a turbine could convert this heat with 35% efficiency. This would imply Valar’s HTGR would need to operate at ~$45-60 per MWh(e). This cost target is in line with estimates from other advanced reactor companies we have done due diligence on. We believe the cost target of a ~$40-50M HTGR is feasible for Valar to achieve. Valar’s material cost estimates provide further support for this conclusion.

Thus we believe it is feasible for Valar to unlock the virtuous cycle of manufacturing reactors to be deployed on Gigasites. This means that Valar could produce ~$1B of revenue (30-45% gross margin) annually per 100 reactors (75 MWth HTGRs) deployed on a Gigasite from synthetic fuels sales. Given nuclear reactors' small footprint, a single Gigasite could host 1000+ reactors, driving $10B+ in revenue per year. With many Gigasites and durable demand for net-zero synthetic fuels (ie. global economic growth), Valar has a path to becoming a $1T company in the decades to come.

Beyond the financial returns of this outcome, we believe Valar success would address two of the largest drivers of volatility globally, energy insecurity and climate change. Since Gigasites could be located anywhere, countries could secure fuel supplies, locking in low prices and minimizing resource wars. Furthermore, Valar could significantly offset otherwise environmentally detrimental consumption of fossil fuels. Simply put, Valar success could be globally important.

Valar’s Leadership & Vision

Valar’s vision is bold. So bold in fact that many will dismiss it before digging in. This would be Valar’s achilles heel if it were not for its founder and CEO, Isaiah. In each of our interactions with Isaiah, we have walked away more impressed than our last. This assessment was unanimous across backchannel references we performed.

Isaiah has a charisma grounded in clear communication that is supported by demonstrated depth and diligence in the complex domain (and history) of nuclear systems. Inspired by Elon Musk, he can be critical and intense. He questions the nuclear industry’s dogmas and will drive his team to achieve what may be unrealistic timelines by industry standards.

Like his reactor company, Isaiah does not fit the standard mold. He is a young, serial entrepreneur that did not graduate from high school. He is however an auto-didact that has shown he can not only develop a business model capable of cutting the Gordian knot that is the advanced reactor industry but recruit the necessary expert talent to make it a reality. Enter Valar’s CNO, Mark.

Mark is a world leading nuclear engineer that has already designed similar nuclear systems to Valar’s TRISO fueled HTGRs at both Ultra Safe Nuclear and the Pebble Bed Modular Reactor project in South Africa (which was being designed to power the previously mentioned SASOL facility’s fuel synthesis). He is even a member of the Nuclear Codes & Standards Committee of the American Society for Mechanical Engineers for HTGRs. You could say he “wrote the book” on the core reactor technology Valar is developing.

Reactors Designed by Valar’s CNO (Pebble Bed Modular Reactor and Micro Modular Reactor)

Beyond Mark’s technical credentials, he is capable of communicating highly technical information at the appropriate resolution, which is often a challenge for the technically inclined. His previous experience running nuclear design teams gives us confidence that when combined with Isaiah’s charisma and ability to make critical decisions, they will be able to recruit and lead a strong team capable of delivering on Valar’s mission.

We are excited to back Isaiah, Mark, and the Valar team in this endeavor.